Generally speaking, FIFO is preferable in times of rising prices, so that the costs recorded are low, and income is higher. Contrarily, LIFO is preferable in economic climates when tax rates are high because the costs assigned will be higher and income will be lower. That means the first 10 shirts you sold were those you bought in January, which cost you $50 each. The last two shirts sold (for a total of 12) were from February, which cost you $60 each. FIFO is an inventory costing method where businesses calculate their cost of goods sold. Now, let’s assume that the store becomes more confident in the popularity of these shirts from the sales at other stores and decides, right before its grand opening, to purchase an additional 50 shirts.

Improve Inventory Management with FreshBooks

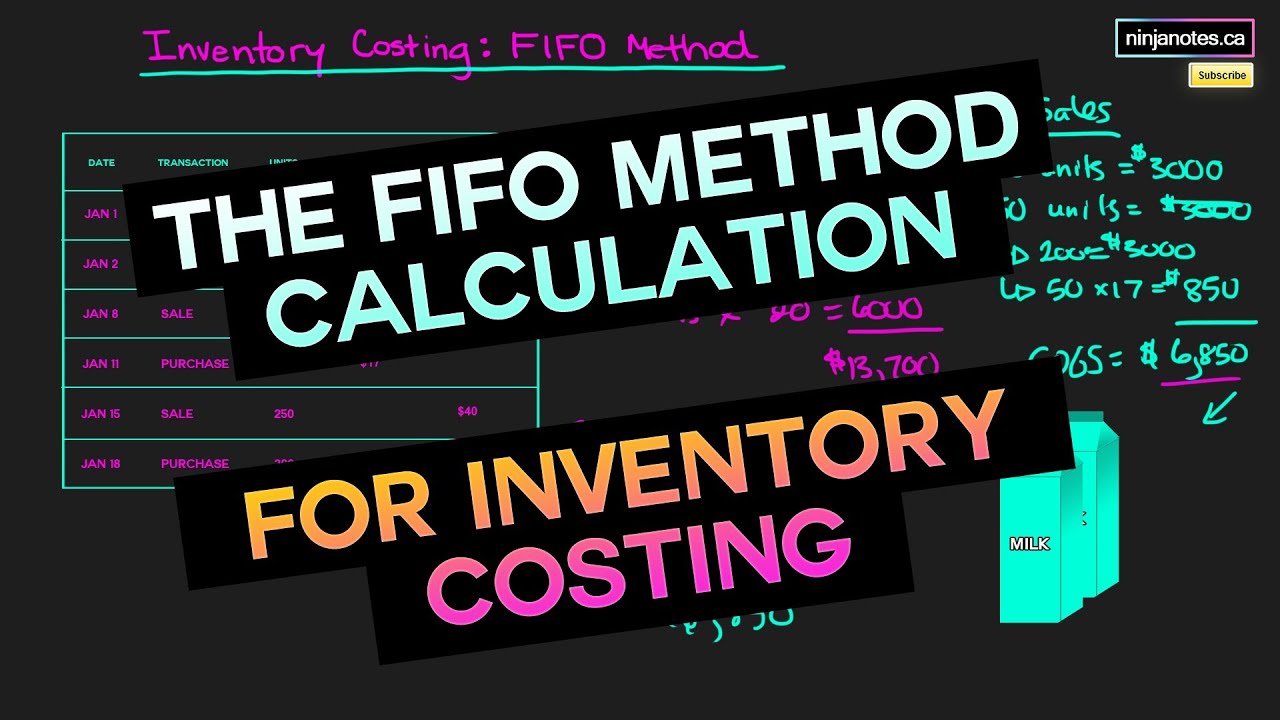

Using FIFO does not necessarily mean that all the oldest inventory has been sold first—rather, it’s used as an assumption for calculation purposes. Learn more about what FIFO is and how it’s used to decide which inventory valuation methods are the right fit for your business. FIFO, or First In, First Out, is an inventory valuation method that assumes that inventory bought first is disposed of first. FIFO has advantages and disadvantages compared to other inventory methods.

Do you already work with a financial advisor?

The FIFO method has advantages for small business owners, especially those who sell items with expiration dates. FIFO accounting is the most commonly used inventory costing method for new businesses. We’ll explore the differences between FIFO and LIFO inventory valuation methods and their relationship to inventory valuation, inflation, reporting, and taxes. We’ll also examine their advantages and disadvantages to help you find the best fit for your small business.

Is FIFO a Better Inventory Method Than LIFO?

This will provide a more accurate analysis of how much money you’re really making with each product sold out of your inventory. Grocery store stock is a common example of using FIFO practices in real life. A grocery store will usually try to sell their oldest products first so that they’re sold before the expiration date.

Which of these is most important for your financial advisor to have?

FIFO and LIFO are two common methods businesses use to assign value to their inventory. They’re important for calculating the cost of goods sold, the value of remaining inventory, and how those impact gross income, profits, and tax liability. Keeping track of all incoming and outgoing inventory costs is key to accurate inventory valuation.

Let’s say that a new line comes out and XYZ Clothing buys 100 shirts from this new line to put into inventory in its new store. Sal’s Sunglasses is a sunglass retailer preparing to calculate the cost of goods sold for the previous year. On the basis of FIFO, we have assumed that the guitar purchased in January was sold first.

- LIFO, or Last In, First Out, is an inventory value method that assumes that the goods bought most recently are the first to be sold.

- In the FIFO Method, the value of ending inventory is based on the cost of the most recent purchases.

- A member of the CPA Association of BC, she also holds a Master’s Degree in Business Administration from Simon Fraser University.

- The reverse approach to inventory valuation is the LIFO method, where the items most recently added to inventory are assumed to have been used first.

This is achieved by valuing the outstanding inventory at the cost of the most recent purchases. The FIFO method can help ensure that the inventory difference between balance b f and balance c f explained is not overstated or understated. In this process, the oldest inventory your business purchases is treated as the first inventory sold.

The most significant difference between FIFO and LIFO is its impact on reported income and profits. For FIFO, higher gross income and profits may look more appealing to investors, but it will also result in a higher tax bill. Under LIFO, lower reported income makes the business look less successful on paper, but it also has a lower tax liability. The type of inventory that a business holds can influence its choice of FIFO or LIFO.

In most companies, this assumption closely matches the actual flow of goods, and so is considered the most theoretically correct inventory valuation method. The FIFO flow concept is a logical one for a business to follow, since selling off the oldest goods first reduces the risk of inventory obsolescence. As the price of labor and raw materials changes, the production costs for a product can fluctuate.